CommSec

CommSec

10 May 2023

Australia’s first budget surplus in 15 years

The federal budget is both an economic and political document. The government of the day outlines the measures that it believes are important for the short and medium-term health of the economy. But given the absence of a majority in the Senate, this means that the government needs to seek agreement with other parties for the measures to become law.

Federal Treasurer Jim Chalmers has forecast a federal budget surplus of $4.2 billion in the 12 months to June 2023, the first surplus since 2008. Australia’s incredibly strong labour market, which has seen unemployment near 50-year lows, combined with higher corporate taxes and income from elevated commodity prices has swelled the Albanese government’s coffers.

The complication this year is that the Reserve Bank is tightening monetary policy to bring down inflation and the community is crying out for support to alleviate cost of living pressures. In other words, Federal Treasurer Jim Chalmers is tasked with delivering credible fiscal management, while supporting society’s most vulnerable at a time when price pressures remain acute, interest rates are at 11-year highs and economic growth is slowing. Ensuring that fiscal policy doesn’t interfere with monetary policy in the fight against inflation has been a key focus of this year’s budget.

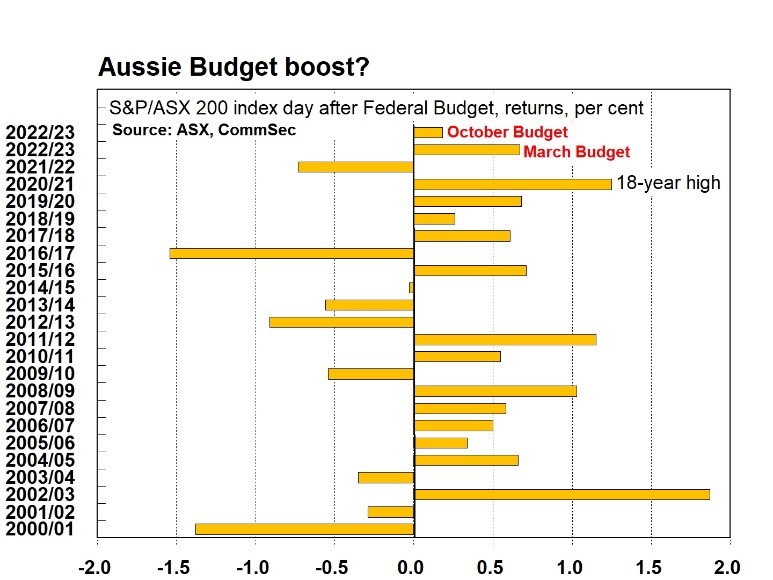

Prior to the pandemic, budgets had limited financial market impact with the 2020/21 budget a standout for supporting consumer and business sentiment during the height of Covid-19 lockdowns. The benchmark S&P/ASX 200 index jumped 1.25 per cent on October 6, 2020 – the day after the budget and the most in 18 years – amid material fiscal stimulus and support for the economy.

In contrast, fiscal austerity in 2014 had the opposite effect on equity market positioning. For investors the important issue is to identify the measures affecting listed companies – either directly or through the effects of budget measures on the broader economy. In particular, the budget policies listed below are expected to have the most impact on the energy, property, healthcare and materials sectors of the Aussie sharemarket.

Cost of living package dominates attention

The cost of living package is the centre-piece of the 2023 budget. While likely to be well received by the community, the risk is that consumer savings are spent, boosting demand for goods and services and slowing the pace of disinflation. Higher interest rates for longer would be negative for consumer and housing dependent companies.

Sharemarket implications

Measure: Cost of living relief package - could boost consumer spending on electronics, clothing and groceries.

Key sectors affected: Consumer Discretionary; Consumer Staples (includes Myer, Harvey Norman, Premier Investments, Super Retail, JB Hi Fi, Coles, Metcash and Woolworths.)

The Federal Government will introduce measures to reduce the cost of living, totalling $14.6 billion over four years.

Analysis: The measures include welfare payments for the unemployed and single parents ($1.9 billion); one-off energy bill discounts ($3 billion); cheaper prescription drugs ($1.6 billion). The cost of living package is in addition to the previously announced reduction in childcare fees ($5 billion) and wage increases in the aged care sector ($14.1 billion).

Jobseekers, those on Youth Allowance and students will get a boost of $40 a fortnight. And around 1.1 million people will receive a boost to rental assistance rates.

Gas reforms with along with energy bill relief are expected to reduce inflation by 3/4 of a percentage point in 2023–24.

Still, on the other side of the equation, any savings generated for consumers may be spent elsewhere. And depending on where the dollars are directed, that may have the effect of pushing prices higher.

The supermarkets may be impacted by a switch away from ‘home brands’ back to named brands. And if people have more dollars in their pockets that may favour café, restaurant and take-away than meals at home.

Cost of living relief may see more dollars being spent on discretionary items at department and electrical and housing-dependent retailers.

Measure: Increase in the Petroleum Resources Rent Tax (PRRT)

Key sectors affected: Energy (Woodside Energy, Beach Energy and Santos)

The proposed increase in the PRRT is expected to generate $2.4 billion in revenue over four years.

Analysis: The increase in the PRRT was first flagged on March 31, so the measure has been largely absorbed by the market. In fact, shares of Liquefied Natural Gas (LNG) producers jumped over 2 per cent on May 8, following the pre-release of the policy ahead of the budget, which showed that the government has adopted more favourable-than-expected changes to the policy. The policy, which increases the tax paid by the offshore LNG industry, is seen as being more equitable across the industry and not impacting growth projects.

The only uncertainty is Coalition views on the change. If there is any solace for LNG producers it is that the federal government could have gone further. The Australian Financial Review notes “Two other options canvassed by Treasury could have raised between $13.3 billion and $21.9 billion from five major offshore gas projects over 10 years to 2033-34, under a $US92-a-barrel ‘‘high price’’ oil scenario.”

The government is effectively raising extra taxation revenue from oil and gas producers and re-directing it to provide cost of living relief for ordinary Australians. The policy also provides greater certainty for the industry in considering future investment in Australia.

Measure: Spending on Defence following Strategic Review and AUKUS submarines deal

Key sectors affected: ASX-listed companies Austal, Codan, Droneshield and Electro Optic Systems are key defence-orientated companies. Also, Materials, Industrials and Communications companies could benefit.

Previously announced measures. Includes re-direction of savings from Defence to the AUKUS program. The recently announced $368 billion submarine deal could benefit engineering companies involved in government contracts, shipbuilders, construction companies, education and communications providers.

The government is also set to spend $400 million to support the retention of Australian Defence Force members via a bonus for personnel who sign on for another term of employment.

WA-based shipbuilder Austal, engineering giant Downer EDI, shipyard builders Boral and Adbri, steel producer Bluescope, Adelaide-located defence electronics and communications Codan and international skills expert IDP Education could all be beneficiaries of these announcements.

Analysis: The changes in the Defence portfolio have dominated news flow over the past few months.

Measure: 15 per cent pay rise for aged care workers at a cost of $11.3 billion over four years

Key sectors affected: Healthcare, Consumer Staples and Consumer Discretionary

Has been previously been flagged. Aged care providers Estia Health and Regis Healthcare shares could lift on increased spending and support for the aged care industry.

Analysis: Inflationary expectations would be limited provided that the pay rise doesn’t cascade to other sectors.

Measure: Review of $120 billion infrastructure project list.

Key sectors affected: Materials, Industrials, Property

The review has been previously announced, but confirmation in the budget of a scaling-back of the Coalition’s sizeable infrastructure program could weigh on building materials, residential and commercial property developers, such as Transurban, Adbri, Bluescope Steel, Boral, Brickworks, Cimic, James Hardie, Mirvac and Stockland.

Analysis: Has regional implications depending on what projects eventually go ahead.

Measure: Net migration target of 315,000 in 2023/24 after 400,000 increase in 2022/23.

Key sectors affected: Real Estate, Consumer Discretionary, and Consumer Staples

The population boom could benefit consumer discretionary and consumer staples stocks, which includes supermarkets and electronics retailers, such as JB Hi-Fi, Harvey Norman, Premier Investments, Metcash, Coles, Wesfarmers and Woolworths, could be beneficiaries of increased consumer spending.

Analysis: Australia needs foreign workers to fill a raft of positions. More people means greater demand for houses, consumer durables like fridges and everyday items like groceries. While the extra workers lift the supply of labour they also increase the demand for goods and services. The net effect on inflation is difficult to estimate. But by not lifting migration either the work wouldn’t be done or the pressure on wages and prices may have increased even more.

Measures: Affordable housing

Key sectors affected: Industrials, Materials, Real Estate (Simonds Group, Mirvac, Lend Lease, and Stockland)

Establishing a new Investment Fund – the Housing Australia Future Fund (HAFF) to boost the supply of, and better facilitate private investment into, social and affordable housing.

Increase the National Housing Finance and Investment Corporation's liability cap by $2 billion to a total of $7.5 billion.

Tax breaks to ensure more investment in build-to-rent projects. Expand eligibility for First Home Guarantee and Regional First Home Buyer Guarantee.

Building materials, residential and commercial property developers could be in focus alongside property-listing firms REA Group and Domain.

Analysis: More activity for home builders and building material suppliers.

Measure: Childcare subsidy

Key sectors affected: Consumer Discretionary (Mayfield Childcare, 3P Learning, G8 Education, Think Childcare, and Kip McGrath Education Centres).

Child Care Subsidy to cost $55.31 billion over four years, up $9 billion.

Analysis: Increased demand for childcare operators.

Measure: Electrification incentives for small business, low income households and renters

Key sectors affected: Consumer Discretionary (retailers, Breville, Shriro).

$1.3 billion in the Household Energy Upgrades Fund to incentivise energy saving upgrades for households and social housing and provides a further $310.0 million in support through the Small Business Energy Incentive.

Analysis: Increased spending on cooktops, heating/cooling systems.

Measure: $5.7 billion to Strengthen Medicare including bulk billing incentives.

Key sectors affected: Healthcare (Ramsay Health Care; Sonic Healthcare; Healthia; Capitol Health).

Take pressure off hospital system; primary healthcare package; GP incentives; boost number of nurses

Analysis: Announced April 28.

Measure: $2 billion for the renewable hydrogen sector

Key sectors affected: Energy and Materials

Analysis: The government is backing the renewable hydrogen sector with $2 billion for the Hydrogen Headstart program to support large-scale projects, in a bid to “bridge the commercial gap for early projects.” It’s also legislating for a National Net Zero Authority to assist with the economic transformation associated with achieving net zero emissions.

Key green hydrogen producers that could benefit from the transition to green hydrogen include: Fortescue Metals Group, Origin Energy, Global Energy Ventures, Lion Energy, Montem Resources, Province Resources and QEM.

Measure: An extra $1 billion for farmers to boost biosecurity measures to keep damaging diseases out of the country.

Key sectors affected: Agribusiness and Materials (Elders, Australian Agricultural Co and Graincorp)

Analysis: Primary producers should benefit from the government’s commitment of an extra A$1 billion to biosecurity measures to fight diseases. Foot and Mouth and other diseases threaten Aussie livestock. The government is also providing extra funding to the Pacific Labour Mobility program, which is designed to help ease worker shortages

Analysis: Protecting Australia’s agribusiness and primary producers remains a priority.

Measure: Visa applications and passenger movement charges will be increased raising $1.1 billion in the five years from 2022/23.

Key sectors affected: Travel (Flight Centre, Qantas, Virgin Australia, Regional Express, Corporate Travel Mgt.)

Analysis: Visitor, working holiday, training and some other visa application fees are going up 15 percentage points, while business innovation and investment visa application fees will rise 40 percentage points, according to budget papers. The Passenger Movement Charge, levied when people leave Australia on international flights or boats, will rise from $60 to $70 per passenger.

Analysis: A steep increase in visa costs and travel fees at a time of acute skilled worker shortages.

Measure: Businesses writing off assets

Key sectors affected: Consumer Discretionary. ASX-listed car dealership and leasing groups like Eagers Automotive, Autosports Group, carsales.com, Eclipx and Peter Warren Automotive.

Analysis: The small business instant-asset write-off has been extended for the 2023-24 financial year, allowing small businesses with an annual turnover of less than $10 million to immediately deduct certain assets worth less than $20,000. New work vehicles could be a popular option for tradies.

Analysis: Business investment and spending could be supported by the instant asset write off policy.

Sharemarket outlook

Just like other major economies, Australia faces headwinds over the next 6-9 months. Based on current data, the economy is at risk of going backwards in the March quarter. Listed companies have acknowledged that while business activity has been generally positive so far in 2023, the second half of the year will be much more challenging.

Aussie investors have focused on the release of third quarter trading updates and earnings over the past 2-3 weeks. The results have been received positively by the market, with Goldman Sachs analysts estimating that the average stock has outperformed the S&P/ASX 200 benchmark index by around 60 basis points on the day of their release. But the benchmark index has declined for three successive weeks. In fact, a handful of stocks have performed poorly following the release of their updates, including Amcor, NAB, ARB Corp, oOh!media and PolyNovo.

Global worries about the potential for an economic downturn, uncertainty around US regional banks, the US debt ceiling, escalating geopolitical tensions, subdued Chinese consumer spending, slowing factory activity, elevated inflation and higher interest rates have combined to dampen risk sentiment.

CommSec’s view is that restrained government spending, rising interest rates, soaring inflation and slowing economic growth all present near-term challenges to Aussie shares.

In this environment, the outlook for Aussie earnings growth looks anaemic with the potential for downgrades from the middle of 2023. Profit margin pressures amid higher wage costs, excess inventories and weaker consumer demand point to an eventual earnings correction.

Bloomberg analyst consensus estimates for the S&P/ASX200 FY23 (2022/23 year) Earnings Per Share (EPS) growth now stands at 4.4 per cent and -1.1 per cent in FY24, following recent downgrades. And on the valuation side, the ASX 200 Price-Earnings (P/E) ratio is now at 14.3x, now below the long-run average.

But while earnings downgrade momentum is expected to intensify over coming months, the decline could be shallower than analysts anticipate. And a policy pause and potential pivot from central banks could coincide with an easing in price pressures. Though, labour market resilience and sticky inflation in the services sector is proving to be a headache for policymakers.

CBA Group economists expect that the RBA ended its hiking cycle in May with the potential for rate cuts in the December quarter, necessitated by a sharp slowing in economic growth after rapid rate hikes. The potential policy pivot and easing of rates could yet support shares into year-end.

Also, Aussie company earnings could be supported by strong population growth and China’s continued economic reopening. The stabilisation in earnings would be positive for travel, education, building and resources companies.

In our view, forward-looking investors are likely to seek out good quality companies with attractive relative valuations in a challenging and uncertain sharemarket constrained by worries about high global recession and earnings risks.

Overall we tip modest growth for the Australian sharemarket in coming months with the S&P/ASX 200 ending 2023 near 7,550 points, up from current levels near 7,300 points.